“The states in the crowdfunding club are red as well as blue, but they share a pragmatism and desire to spur entrepreneurship and job creation within their borders.”

On a cold day in late November, Kyle DeWitt and Tim Schmidt were overseeing the final phase of their longtime dream to open a microbrewery. The brewing equipment was hauled in, the taps were installed, and the electricians were rewiring the renovated historic building in downtown Tecumseh that will be home to Tecumseh Brewing, a brewpub and beer garden that will feature a rotating roster of microbrews, from a Black IPA to a Peanut Butter Stout.

When the taps finally start flowing in January, it will be thanks to a recently passed Michigan law that allows any business based in the state to raise money from any resident of the state through crowdfunding – a form of online fundraising where small sums from a large number of investors take the place of one or two big financiers.

After months of drawn out talks with banks and state funding agencies that seemed to be going nowhere, DeWitt and Schmidt decided last March to give the new law, the Michigan Invests Local Exemption (MILE), a try. They put together a campaign on LocalStake, a crowdfunding platform, and raised $175,000 from 21 local investors. The pair hit their funding goal in half the time allotted and had to turn away investors. The crowdfunding campaign also helped the brewery secure a $200,000 bank loan to complete its funding needs. Without MILE, says DeWitt, “We’d still be banging our heads against the wall.”

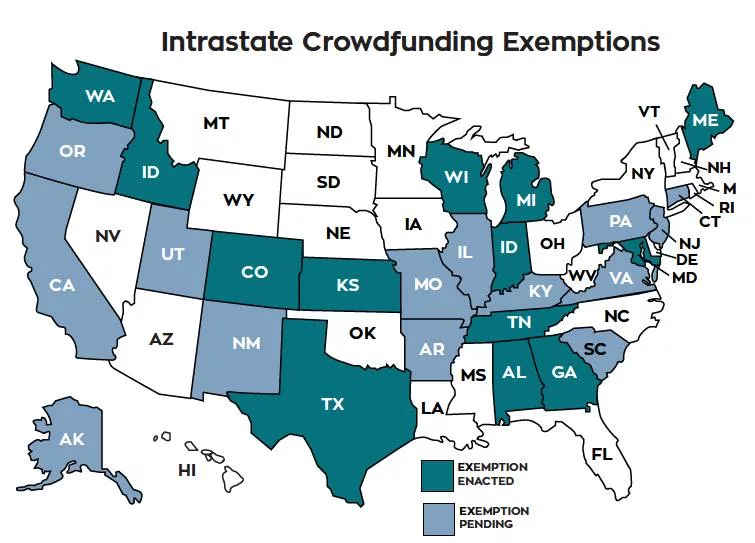

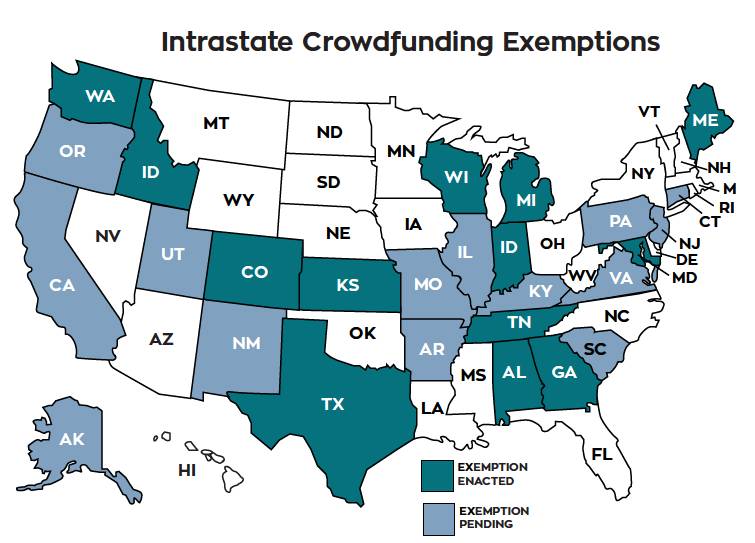

Michigan’s MILE is one of more than a dozen such state laws that have cropped up over the past two years to help get capital into the hands of cash-strapped entrepreneurs. They seek to fill a funding gap for promising local ventures that are not being served by conventional funders like banks and venture capital, which tend to focus on larger, less risky deals.

That was also the aim of the Jumpstart Our Business Startups (JOBS) Act, landmark legislation signed into law by President Obama in April 2012. The centerpiece of the JOBS Act was a crowdfunding provision that would make it easier for small, private companies to raise money by offering equity or debt to investors, including their customers, friends, and the general public. (Securities laws have made it prohibitive for small private companies to raise money from all but the wealthiest investors.) Crowdfunding represented a democratizing force that could unlock new sources of capital for job-creating entrepreneurs, boost the economy, and give Wall Street-wary investors a profitable alternative. The president called it “a game-changer.”

But more than two-and-a-half years later, the crowdfunding law, often referred to as Title III of the JOBS Act, is bogged down in rule-making at the Securities and Exchange Commission. What’s more, the rules as proposed would impose costly requirements on small businesses wishing to raise capital and on crowdfunding platforms alike, causing even the bill’s most ardent supporters to declare it unworkable.

“At the end of the day, Title III is deeply flawed,” said Patrick McHenry, a North Carolina House representative and the original champion of the law.

Against that disheartening backdrop, a growing number of states like Michigan are crafting their own mini-JOBS Acts. Texas became the thirteenth state to pass a state crowdfunding law in November, and Oregon was expected to enact one by the start of the new year.

The states in the crowdfunding club are red as well as blue, but they share a pragmatism and desire to spur entrepreneurship and job creation within their borders.

The laws vary by state and often reflect the unique character of their regions. Vermont’s Small Business Offering Exemption, for example, excludes companies involved in petroleum production, mining, or other extractive industries. Kansas officials, meanwhile, named their law the Invest Kansas Exemption, or IKE, to honor the state’s most famous native, Dwight Eisenhower.

Like the JOBS Act, the state crowdfunding laws include restrictions on how much companies can raise (typically $1 million to $2 million in a year) and how much non-wealthy investors can invest in crowdfunding deals. But generally, they allow any business based in the state to raise money from any resident of the state, without all of the red tape and restrictions that come with the JOBS Act. In Kansas and Georgia, the first two states to enact such laws, companies raising money submit a simple one-page form to state regulators, and there are no audited financials required. There’s not even a requirement for a web portal – companies can raise money completely offline if they wish.

State crowdfunding has its limits. Only companies incorporated in a particular state and doing the majority of their business there are eligible (that means no Delaware corporations). And companies are restricted to raising money from state residents (or face harsh penalties). As such, this approach may not appeal to high-flying firms that can attract a national or global audience of investors. But then, those companies typically have no problem raising capital – unlike the thousands of smaller, community-based businesses that the state laws are intended to help.

Indeed, the promise of intrastate crowdfunding may be greatest in rural areas far from urban money centers like New York or Denver, where communities are struggling to stay relevant and keep their young from leaving. In Kansas,“The theme has been more community development than get rich quick,” says Kansas Securities Commissioner Josh Ney. The eight or so ventures to take advantage of IKE so far have ranged from a dairy farm to a grocery store – and yes, a couple of microbreweries.

Minneola, for example, is a rural farming community of 750 in southwestern Kansas, so small that it didn’t even have a local grocery store. Using the IKE law, local businessmen raised $180,000 to open the Hometown Market, a grocer with a deli, prepared foods counter, and a florist. More than 180 people invested – or one in seven residents. The market is not a huge moneymaker, but it offers a vital service to residents. “It’s more of an investment in the community and a way of life,” explains Luke Jaeger, who serves as chairman of the market.

It’s much the same in Michigan, where several small companies, including a minor league baseball team, a maker space, and a spirits distiller, are preparing to take advantage of the MILE law. Chris Miller, an economic developer in Adrian, Michigan, who was a driving force behind MILE, views it as “a real and significant opportunity to have an impact on a local economy.”

State crowdfunding has been slow to take off – a fact that critics have seized on. But that’s to be expected with a major change in law, and state officials are working to raise awareness and to educate investors and entrepreneurs. Federal regulators have thrown up some roadblocks, too, and there are kinks to be worked out. And yes, there are risks: some people will lose money with crowdfunding, no doubt, just as they do in the stock market or any other investment category.

But it’s a risk worth experimenting with. Just as Kickstarter has allowed independent artists to bypass the traditional gatekeepers like record studios and publishers to get their works produced, crowdfunding can help entrepreneurs with good ideas and promising growth potential get the funding that is denied to them by banks and VCs. Millions of Americans have moved their money out of big banks to credit unions and community banks; many may want to do the same with some of their investment dollars.

As with gay marriage and marijuana, states will be the laboratories where the crowdfunding experiment plays out. “This is something states can take the lead on,” says Commissioner Ney of Kansas. “We want to show the more benevolent side of crowdfunding and that local, community offerings can be successful.”

Amy Cortese is a journalist whose work has appeared in the New York Times, Business Week and other publications. Her book Locavesting: The Revolution in Local Investing And How To Profit From It, helped popularize the concept of community capital. Her latest venture, www.locavesting.com, is a hub for local investing news, education and resources.