Four decades’ worth of growing inequality in income, wealth, and opportunity — and the contraction of the middle-class standard of living — has serious implications for the health of the US economy. While the unemployment rate is low, a closer look reveals a number of troubling indicators, especially a yawning racial divide between White people and people of color. These two trends — the racial wealth divide and growing economic inequality — are often analyzed as separate and merely concurrent. In fact, they are mutually reinforcing outcomes of a larger economic picture.

If the racial wealth divide continues, the economic constraints on Black and Latinx households will drag down America’s overall median wealth for generations. African-Americans and Latinxs already comprise more than 25 percent of the US population. As our country diversifies even further, the systemic obstacles to their wealth-building will result in steadily increasing inequality in the overall population.

Concentration Beyond Comprehension

There are several dimensions to the story of contemporary economic inequality.

Since the late 1970s, real wages have been stagnant for over half of the US workforce. Meanwhile, the cost of housing, health care, and other basic needs have risen. Starting in 2005, the percentage of households that own a home started to decline. These trends touch people of all races, fueling some of the discontent of both regressive and progressive populism.

The 2008 economic meltdown accelerated these trends. Most of the income and wealth gains of the decade since the recession have flowed to the richest one-tenth of the 1 percent, leaving the wealthiest 1 percent of Americans with more wealth than that of the bottom 90 percent of the population combined.

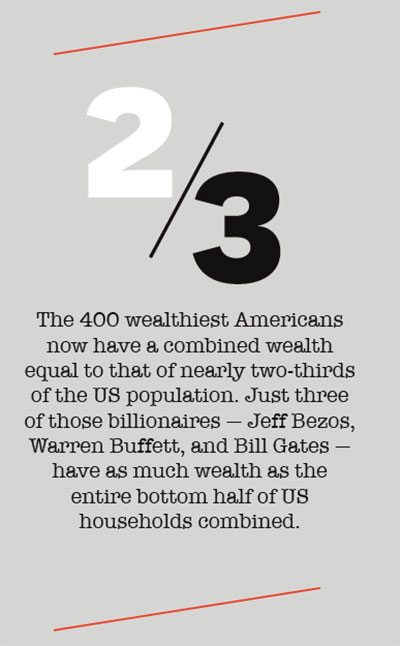

The extent of America’s wealth concentration is difficult to comprehend — or to exaggerate. The 400 wealthiest billionaires in the US now have a combined wealth equal to that of nearly two-thirds of the US population. Just three of those billionaires — Jeff Bezos, Warren Buffett, and Bill Gates — have as much wealth as the entire bottom half of US households combined.

Where Past Meets Present

Inequality is often measured in income, or what people take home from their paychecks. But wealth — the total measure of what you own minus your debts — is a more accurate indicator of a household’s long-term financial stability and wellbeing. Families with more wealth can cover emergencies without going into debt and take advantage of economic opportunity, such as buying a home or saving for college.

Wealth is also where the past shows up in the present. Nationally, measures of wealth reflect the multi-generational story of White advantage and racial discrimination in asset-building.

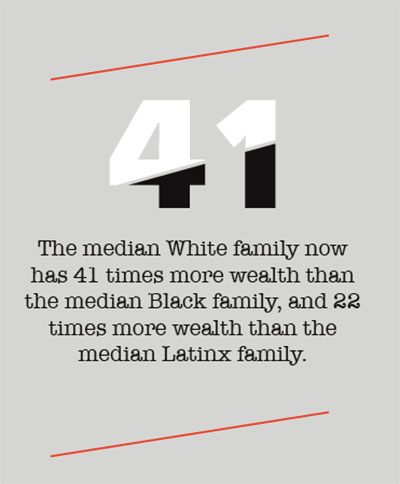

The disparities are nothing short of dramatic. The median White family now has 41 times more wealth than the median Black family, and 22 times more wealth than the median Latinx family. These are among our findings in “Dreams Deferred,” a new study on the racial wealth divide that we co-authored for the Institute for Policy Studies.

Since the early 1980s, median wealth among Black and Latinx families has been stalled at less than $10,000. In fact, the median Black family today owns just $3,600 — that’s 2 percent of the $147,000 the median White family owns. The median Latinx family does little better at $6,600 — just 4 percent of the median White family.

These enormous disparities are key to understanding the decline in median wealth for all US households, which has gone down by 3 percent since 1983. Over this same period, the median Black family saw their wealth drop by more than half.

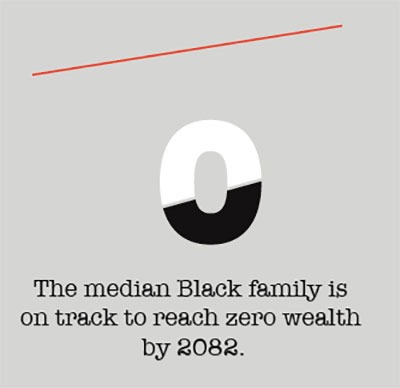

If the trajectory of the past three decades continues, by 2050 the median White family will have $174,000 of wealth, while the median Latinx family’s wealth will be just $8,600 — and the median Black family wealth will head downward to $600. Alarmingly, the median Black family is on track to reach zero wealth by 2082.

While the middle class stagnates and the very richest leave everyone else behind, there’s also growing precariousness at the bottom end of the spectrum. A growing number of households are “underwater” when it comes to wealth. The proportion of all US households of any race with zero or “negative” wealth (meaning their debts exceed the value of their assets) has grown from one in six in 1983 to one in five households today.

Families of color are much likelier to be in this precarious financial situation: 37 percent of Black families and 33 percent of Latinx families have zero or negative wealth, compared with 15.5 percent of White families.

By 2060, the combined Black and Latinx percentage of the population is expected to rise to 42.5 percent. Low levels of Black and Latinx wealth, combined with their growing proportion in the population, are a significant contributor to the overall decline in American median household wealth.

Plainly, these racial wealth divisions are damaging to the economy as a whole.

How This Happened

This disturbing inequity was no accident. It’s the result of systemic factors and deliberate government policies — both past and present. In the overall economy, the growing shift of financial rewards to capital investors, and away from workers, is a key culprit. This creates an increasingly regressive economy that leaves those with few assets further and further behind.

The racial wealth divide, of course, has its own deeply rooted causes. Historically, the divide was maintained even when the economy was going strong and we had progressive investments in lower-income and working-class people.

This racial divide was maintained by excluding African-Americans and other communities of color from public investments. For example, a generation of White families were able to purchase their first home between 1946 and 1966 with government-subsidized mortgages such as those provided by the Farmers Home Administration, Veterans Administration, and Federal Housing Administration insurance programs. People of color were almost entirely excluded from these mortgage programs — and so lost a generation or more of opportunity to build wealth.

Past discriminatory housing policies continue to fuel an enormous racial divide in homeownership rates. Meanwhile, an upside-down tax system helps the wealthiest households (who are overwhelmingly White) get wealthier while providing the lowest-income families (who are disproportionately people of color) with almost nothing.

What Can Be Done

Building an inclusive middle class hinges on our ability to adopt targeted and effective programs that address the specific needs of low-wealth communities. This approach will strengthen the American middle class as a whole and make our middle class much more racially and ethnically inclusive.

Such policies could include the expansion of first-time homeownership initiatives for those who were denied access

to home mortgage financing in the decades after World War II and up to the present. These could include low-interest loans and down-payment assistance.

Additional initiatives could remove barriers to higher education, especially when targeting first-generation college students and low- and middle-income households. Student debt now exceeds $1.5 trillion and interferes with younger people being able to save money, build wealth, and purchase homes.

These should be accompanied by policies to protect low-wealth families from predatory financial practices, including by strengthening the Consumer Financial Protection Bureau. Predatory auto loans, alongside other forms of predatory debt, are on the rise, fueling potential debt bubbles.

Other ideas include generating wealth for all Americans and transferring it to them directly. Senator Cory Booker, for instance, has proposed the creation of a “baby bond” program that would seed an asset account for every newborn.

According to one study, had such a program been in place in 1979, the wealth divide between young Latinx and White households would have been entirely closed by now, and the wealth divide between young Black and White households would have shrunk by 82 percent.

In addition to programs specifically geared towards historically excluded communities, we need others that look to turn our overall economy right-side up — so those in the working and middle classes receive the majority of the growth they help our economy produce.

We could pay for some of these investments by restoring progressiveness to the US tax system and raising rates on the highest brackets to their post-World War II levels. We could also fix some of the upside-down tax incentives that subsidize the already wealthy and direct investment into opportunities for low-wealth families. Specifically, we should reform the mortgage interest deduction (which can favor people with pricey homes at the expense of ordinary people) and other tax expenditures.

Add to all these measures common-sense ideas like raising the minimum wage, expanding health care coverage, and taxing the 1 percent to fund education and infrastructure. Together these ideas wouldn’t just close the racial wealth divide — they’d create an economy that works for all Americans, not just the super-rich.

What We Can Build

The creation of a strong American middle class after World War II didn’t happen on its own. It required a healthy, vibrant economy, including significant investments in the ability of Americans to build lasting financial security through homeownership, higher education, and transportation.

But these policies were most often intentionally directed at White communities and away from Americans of color. We’re committing economic suicide if we continue to exclude the coming majority of the country from opportunities to invest in the future. In this century, America must come together to build — for the first time — an inclusive middle-class economy.